Top 10 Things Every Creditor Should Know About Chapter 11 Bankruptcy

Each year thousands of companies file for Chapter 11 Bankruptcy protection to address their financial difficulties by reorganizing their businesses under the supervision of the bankruptcy court. As opposed to Chapter 7 Bankruptcy that ultimately dissolves a business and is often perceived as failure, a financially distressed company (the Debtor) is able to continue their day-to-day operations while devising a plan to reorganize and become profitable again. Their objective is to re-emerge as a financially healthy, viable business with little to no disruption in their organization’s daily activities.

Chapter 11 presents a unique opportunity for the Debtor, but it can cause a ripple effect of consequences for their customers, vendors, suppliers, partners, lenders, and individuals that have unpaid bills or outstanding invoices. Under Ch.11, these Creditors are lawfully entitled to repayment, and thus have a Bankruptcy Claim against the Debtor in the case. The Bankruptcy Court, the Debtor, and the Creditors all play a part in the process to determine the outcome of the case.

The process of Ch.11 is complicated, extensive, and does not always result in a successful reemergence for the Debtor. However, the process can prove to be even more unpredictable for the Creditors involved. Because of the circumstantial nature of Ch.11 cases, it is beneficial for Creditors to have a thorough understanding of the procedures and key terminology to better navigate the process.

In this article, we’ll walk you through the top 10 things every Creditor should know about the Chapter 11 process.

1. Automatic Stay

From the moment a Debtor files a bankruptcy petition with the court, an automatic stay is enforced. This injunction forbids any Creditors from collecting on outstanding invoices, bills, or other debt they have against the Debtor. The reason behind the automatic stay is to grant the Debtor space and ample time to evaluate their next steps.

If a Creditor has an existing lawsuit, it is not necessary for them to dismiss the case. The automatic stay requires that all collection efforts be suspended. A Creditor can request relief from the injunction to continue their collections. However, it is unlikely for the Bankruptcy Court to approve the requested exception unless the Creditor has a secured bankruptcy claim.

2. Request for Notices

The complexities of the Ch.11 process make it incredibly difficult for a non-lawyer to stay updated on the case proceedings. For this reason, it is highly recommended for Creditors to seek legal counsel to assist them throughout the bankruptcy proceedings. In the event that a bankruptcy attorney is retained, it is important to file a request for notices so that your attorney receives everything filed in the case via email and can keep you informed.

3. Schedule of Liabilities

In the early stages of a bankruptcy case, the Debtor is required to file a Schedule of Liabilities. This step is a key determining factor of the Creditor’s recovery as it will declare the respective categories, amounts, and status of the debts owed to Creditors according to the Debtor’s accounting records.

It is crucial for the Creditor, or their attorney, to review the Schedules and ensure that their Bankruptcy Claim is indeed listed and that the amount is correct. If a Creditor disagrees with how their Bankruptcy Claim is stated in the Schedules or it is not listed at all, they must take immediate action to file a Proof of Claim to the court in order to assert their legal right to payment. Without doing so, the Creditor runs the risk of having the Debtor’s filed records act as the basis for their eventual claim payment.

4. Filing an official Proof of Claim

If a Creditor’s Bankruptcy Claim is not listed or listed inaccurately in the Debtor’s Schedules, the Creditor must file an official Proof of Claim to exercise their rights to receive the correct amount from the Debtor. This is also a necessary step if the listed Bankruptcy Claim happens to be categorized as disputed, contingent, or unliquidated. The Proof of Claim must be filed with supportive documentation as evidence to back up the validity of the bankruptcy claim. It is crucial that the Proof of Claim is filled out to completion and submitted on time. However, Creditors are allowed to revise their original Proof of Claim, if they’ve discovered a mistake or additional debt, by filing an amendment.

5. The Bar Date

All Creditors will receive the Notice of the Bar Date when they receive their formal Notice of Bankruptcy in the mail. The Bar Date is the final court deadline for Creditors to submit their Proof of Claim against the Debtor. Proofs of Claim that are submitted after the Bar Date are rejected by the court and will not be taken into account in the case.

6. First Day Motions

Another key point of the Chapter 11 process occurs shortly after the Debtor files its bankruptcy petition. The Debtor files what is referred to as “first day motions”, which allow the company to continue its operations. The first day motions often include requests for legal and financial advisors, the use of cash collateral, and the approval of financing for maintaining control of their business and the decision making.

7. Use of Cash Collateral

When the Debtor needs to use borrowed cash during a Ch.11 case, it is referred to as cash collateral—cash receivables and equivalents secured by Debtor property as collateral. This might include liens on real estate, documents of title, deposit accounts or other accounts receivable. The use of cash collateral should be stated in the Debtor’s first day motions with a budget.

When a Debtor files for Ch.11, they are permitted to use the cash collateral with either court approval or permission of the Lender or Secured Creditor. It is important to note that the use of the cash collateral can result in the secured Creditor being entitled to additional compensation for the loss of value that it has provoked.

8. Reclamation Rights

Reclamation is the assertion of a vendor or seller’s right to reclaim any goods sold to the Debtor during the time that it was bankrupt. This process is specifically outlined in the Bankruptcy Code for these Creditors to fully understand how to reclaim their goods. The time allotted for acting upon this reclamation right is slim, so it is important for Creditors encountering this situation position to act quickly with their legal counsel.

9. Executory Contracts

Executory contracts can be advantageous for the Creditor when their customer files for Ch.11 Bankruptcy. This refers to a contract under which both parties still have obligations to perform.

Debtors in possession can assume or reject an executory contract, meaning a Debtor can decide to keep an existing contract or choose to terminate it. The Debtor has the duration of the case to make these decisions. However, the assumption or rejection of a contract must be approved by the Bankruptcy Court.

Upon assumption of an executory contract, the Debtor is required to pay the full value of the Bankruptcy Claim when the case is filed or propose a payment plan. Under these circumstances, the Creditor must continue to perform under the terms of the assumed contract, while the Debtor continues to provide compensation for their work throughout the pendency of the Bankruptcy Case.

Leases can be considered executory contracts and can even have more special protections than others. In regards to unexpired leases for non-residential properties, landlords often have a better deal. The Debtor has 120 days to decide if it plans to assume or reject the non-residential lease. If they fail to act by the deadline, a landlord can expect their lease to be rejected and thus terminated.

10. Plan of Reorganization

One of the most important aspects of Ch.11 Bankruptcy for Creditors to recognize is the fact that payment is not guaranteed. Even if a Creditor files their Proof of Claim on time, to completion, and accurately, there are several steps along the way that can hinder their chances of recovering their lost revenue.

Under the Ch.11 process, the Debtor is given the opportunity to formulate what is called a Plan of Reorganization that outlines the restructuring steps they commit to take in order to pay back their debts and reorganize their business. The Plan of Reorganization will determine which Creditors are guaranteed payment and the order in which payments will be distributed by categorizing the allowed Bankruptcy Claims into different classes.

Creditor classes are determined by whether a Bankruptcy Claim is secured or unsecured. Secured Claims are supported by a form of collateral or contractual agreement and have the highest priority level, which means such Creditors are guaranteed to be paid first and in full before any others. General Unsecured Claims, however, risk the possibility of receiving no payment, only a portion of their Claim value, or distribution of another form.

Once the Debtor submits the Plan of Reorganization, it is reviewed by both the Bankruptcy Court and the various Creditor classes. A hearing is held with the court to examine the documents. At this point, the Court can file any objections they have to the Plan. With Court approval, the eligible Creditors then vote on whether to approve or reject the plan.

The votes are then tallied and another hearing is scheduled to determine the final outcome of the Ch.11 case. If the voting leans in favor of the Plan, objections have been settled, and the court decides everything is in line with the bankruptcy code, the Plan of Reorganization is confirmed and a “plan effective date” is scheduled for the implementation of the Plan. With a confirmed Plan of Reorganization, the Debtor is able to emerge from Chapter 11, pay back its Creditors, and operate as a financially stabilized business.

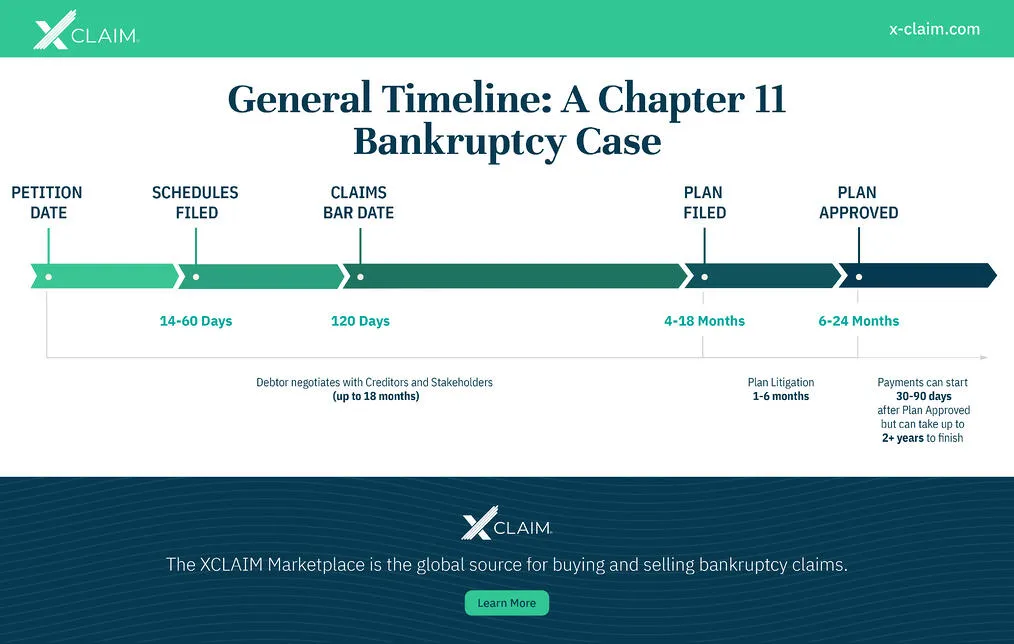

Timing Can Vary

Every bankruptcy case is uniquely nuanced. The following diagram illustrates what the process might look like for a "typical" case to conclude. Because many complex factors affect the timing and unpredictability of the court process, it is best to remain patient and to stay informed.

The Bottom Line…

While filing for Ch.11 Bankruptcy provides an opportunity for Debtors to dig themselves out of the financial distress they have found themselves in, the process can have varying consequences for the Creditors involved. Depending on whether or not the nuances of the bankruptcy proceedings lean in their favor, Creditors can fall victim to these unfortunate circumstances and find themselves in a similar distressed position when claims go unpaid.

The good news, however, is Creditors can take an alternative route to recovery and receive immediate liquidation of their Bankruptcy Claim. The industry of Claims Trading has existed for several decades and has recently been made more accessible, efficient, and convenient. It is no longer necessary for Creditors to wait around trying to predict the outcome of an incalculable Chapter 11 Bankruptcy case.